08 Jun How does Credit Score work?

Getting the facts straight about credit restoration and the credit industry can be a daunting task. There is a lot of misinformation about credit and many people are under the impression that there is nothing they can do to fix their credit score.

We are here to educate you about credit, so you won’t be in the same situation again. Our goal is to help you improve your credit score and maintain it. Learning about your credit and how it affects many aspects of your life is the first step towards improving it.

With so much emphasis on your credit score, it is important to understand how the score is calculated. Commonly referred to as your FICO Score, your credit score is a summation of complex algorithms used to determine your exact score. While the formulas are protected, we are given approximate percentages that help us understand what goes into your score.

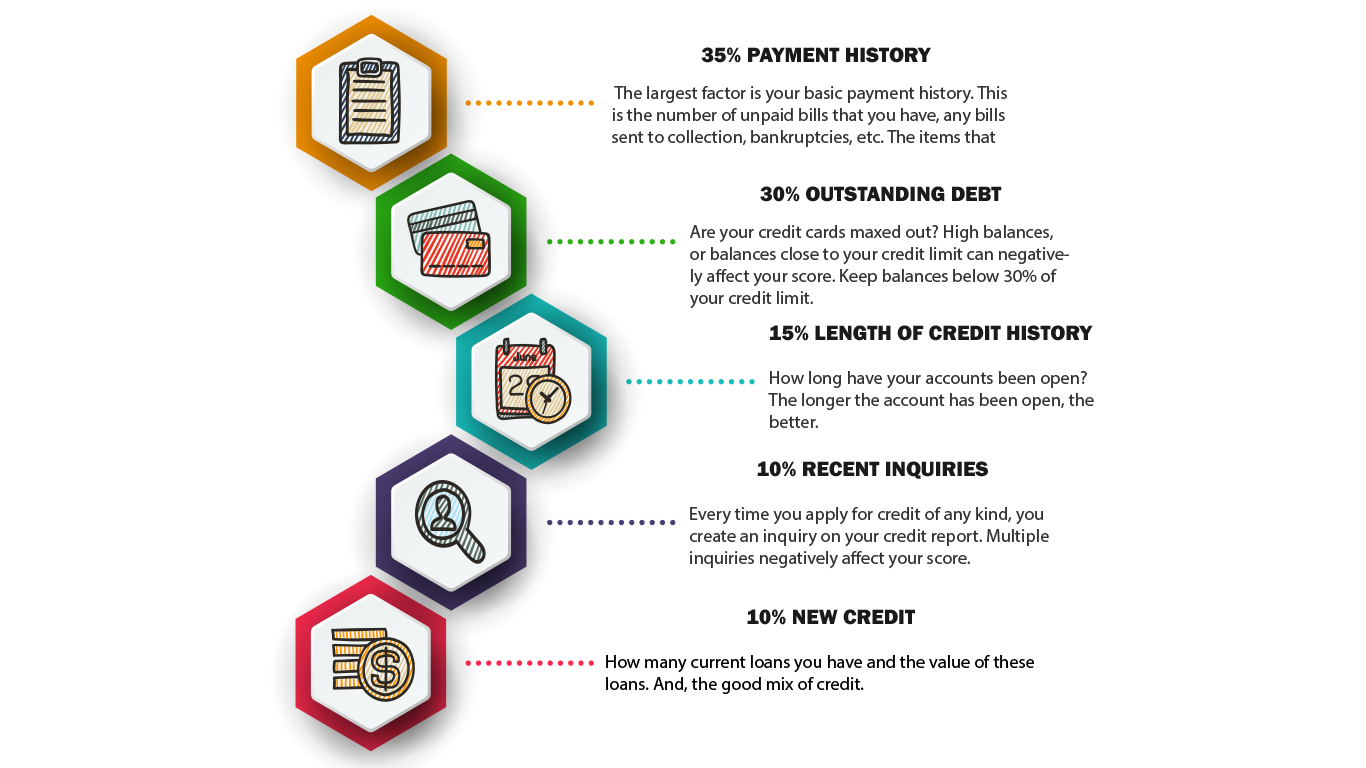

- 35% PAYMENT HISTORY – The largest factor is your basic payment history. This is the number of unpaid bills that you have, any bills sent to collection, bankruptcies, etc. The items that are most recent have the most impact.

- 30% OUTSTANDING DEBT – Are your credit cards maxed out? High balances, or balances close to your credit limit can negatively affect your score. Keep balances below 30% of your credit limit.

And the better your scores get the lower this ratio should be, and the ideal is under 10-15% of each credit limit and total credit limits

- 15% LENGTH OF CREDIT HISTORY – How long have your accounts been open? The longer the account has been open, the better.

- 10% RECENT INQUIRIES – Every time you apply for credit of any kind, you create an inquiry on your credit report. Multiple inquiries negatively affect your score.

- 10% NEW CREDIT – How many current loans you have and the value of these loans. And, the good mix of credit.

A perfect credit report has a few credit cards, one or two instalment loans (mortgage or car loan)

If you don’t have any open credit card, or any open instalment loan, your score will not increase.

Three major bureaus dominate the market for supplying American lenders with credit scores. When you apply for credit, it does not come directly from FICO;( because it is only an algorithm which the bureaus Must pay for), because of that and other reasons, each bureau has its own version with its own name.

If you have any questions or think that we can help you, Baby Boomers is here for you Call Us Today! (833)700-6835 or send us a message here!